Tuesday, March 12, 2024

Saturday, February 24, 2024

Commodities Entry points

NATGAS (ET PAA KMI NWN ENB ) , Grains and Corn managed-money futures positions (hedge funds) have reached the most extreme net short (vs. open interest) since 2006. Diminishing bear market room in corn (grains) may be turning attention toward crude oil. Courtesy: McGlone BI posts.

On a separate note -

While these returns may appear modest in today’s speculative environment, such movement in a macro asset of this magnitude could unleash other important trends that are long-overdue.

Currently priced for failure, the mining industry stands out as one of the best distressed opportunities, in my view. Additionally, it's worth noting that historically, every gold cycle has synchronized with a cycle for other commodities, often boosting the valuations of resource-rich economies like emerging markets.

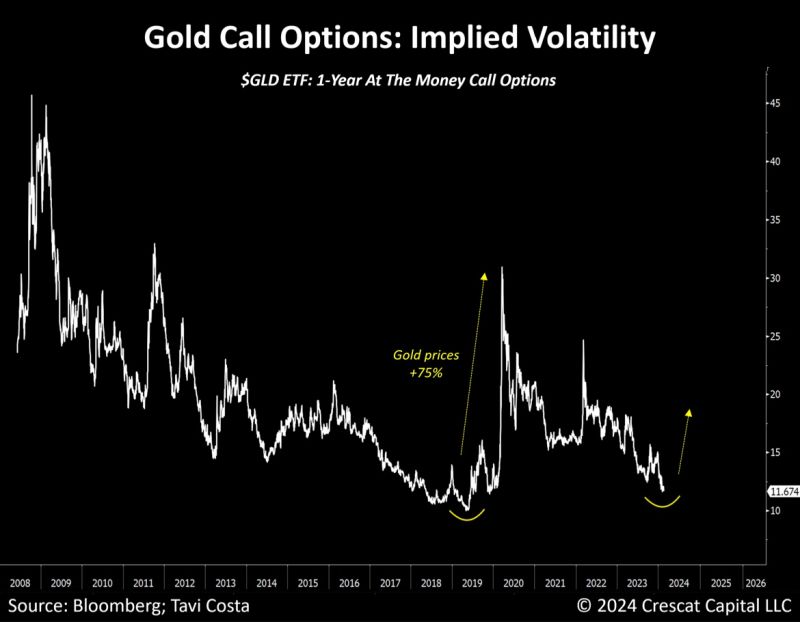

The drop in implied volatility of call options on gold to historically low levels may signal an upcoming surge in gold prices, potentially impacting the mining industry and related markets. Here are the key points to consider:

- Historically, low volatility in gold options has been followed by substantial price increases, given gold's role as a major macro asset.

- The undervalued mining industry may see growth if gold prices rise, offering potentially high returns for investors.

- Gold cycles have historically impacted broader commodity cycles, driving up the value of resource-rich economies.

- Increasing exposure to gold and related industries could provide portfolio diversification and help manage risk during uncertain economic periods.

In summary, this situation may present promising investment opportunities in the mining industry and related markets. It's important to conduct thorough research and assess individual risk tolerance before making any investment decisions.

- Historically, low volatility in gold options has been followed by substantial price increases, given gold's role as a major macro asset.

- The undervalued mining industry may see growth if gold prices rise, offering potentially high returns for investors.

- Gold cycles have historically impacted broader commodity cycles, driving up the value of resource-rich economies.

- Increasing exposure to gold and related industries could provide portfolio diversification and help manage risk during uncertain economic periods.

In summary, this situation may present promising investment opportunities in the mining industry and related markets. It's important to conduct thorough research and assess individual risk tolerance before making any investment decisions.

Lastly, the delinquencies are at 20 year high.

Massive insider sells across the board -

WMT Insiders sold, JPM's Dimon sold, Bezos sold

Saturday, August 26, 2023

Good Entry points !!

DIS

IFF

PYPL

SQ

CCJ

Oil ( OIH upstream pipelines) & Gas (XOM CVX) , CLB, FTK?

Silver (sivr)

Gold (NEM RGLD)

MMM (?)

ABNB

Monday, January 18, 2021

Reaching Euphoria - all time highs...

The markets have rallied substantially since the March'20 bottom. SPACs, IPOs craze is visible in all forums, especially fueled by the new generation of Robinhood traders. Tiktok videos are being made on stock trading. Youtube channels are pumping names and creating significant moves. These are unprecedented times where stimulus money is flowing in - the traders are buying/selling without commissions, and their relatively young age guarantees that they've not had major learnings of how the market forces truly work. The new normal due to fed put and unlimited QE and stimulus has run it's course and may inflate the tulip bubble even further - no one can time a top. Nevertheless, the charts and the sentiments are definitely flagging caution.

Wednesday, January 15, 2020

Correction scoops

https://etracs.ubs.com/product/list/index/strategy/income ; APLE, CIM, BDCs,

AAPL

WDAY

TSLA

AMT

MSFT

IBM

ABBV

DXCM

COUP

BIDU

PINS

MU

AMD

NVDA

XLNX

SBAC

LRCX

SKYW

TSM

MOS

XOM

AAPL

WDAY

TSLA

AMT

MSFT

IBM

ABBV

DXCM

COUP

BIDU

PINS

MU

AMD

NVDA

XLNX

SBAC

LRCX

SKYW

TSM

MOS

XOM

Tuesday, May 7, 2019

IPOs May 2019

Wednesday, March 27, 2019

100 IPO list - March 2019

| Symbol | Company | Industry | Offer Date | Shares (millions) | Offer Price | 1st Day Close |

| LEVI | Levi Strauss & Co. | Consumer Goods | 3/21/2019 | 36.7 | $17.00 | $22.41 |

| TIGR | UP Fintech Holding Limited | Financials | 3/20/2019 | 13 | $8.00 | $10.92 |

| FHL | Futu Holdings Limited | Financials | 3/8/2019 | 7.5 | $12.00 | $15.32 |

| SWAV | ShockWave Medical | Health Care | 3/7/2019 | 5.7 | $17.00 | $30.50 |

| KLDO | Kaleido Biosciences | Health Care | 2/28/2019 | 5 | $15.00 | $14.23 |

| SLGG | Super League Gaming | Consumer Services | 2/26/2019 | 2.3 | $11.00 | $8.50 |

| HOTH | Hoth Therapeutics | Health Care | 2/15/2019 | 1.3 | $5.60 | $8.53 |

| AVDR | Avedro | Health Care | 2/14/2019 | 5 | $14.00 | $12.29 |

| TCRR | TCR2 Therapeutics | Health Care | 2/14/2019 | 5 | $15.00 | $15.07 |

| HARP | Harpoon Therapeutics | Health Care | 2/8/2019 | 5.4 | $14.00 | $13.50 |

| ALEC | Alector | Health Care | 2/7/2019 | 9.3 | $19.00 | $18.00 |

| NFE | New Fortress Energy | Oil & Gas | 1/31/2019 | 20 | $14.00 | $13.07 |

| MTC | MMTEC | Technology | 1/8/2019 | 1.8 | $4.00 | $5.94 |

| QFIN | 360 Finance | Financials | 12/14/2018 | 3.1 | $16.50 | $16.50 |

| TME | Tencent Music Entertainment Group | Consumer Services | 12/12/2018 | 82 | $13.00 | $14.00 |

| MRNA | Moderna | Health Care | 12/7/2018 | 26.3 | $23.00 | $18.60 |

| THOR | Synthorx | Health Care | 12/7/2018 | 11.9 | $11.00 | $12.61 |

| MOGU | MOGU | Consumer Goods | 12/6/2018 | 4.8 | $14.00 | $14.00 |

| MDRR | Medalist Diversified REIT | Financials | 11/28/2018 | 0.2 | $10.00 | $9.40 |

| TC | TuanChe Limited | Consumer Goods | 11/20/2018 | 2.6 | $7.80 | $7.83 |

| BCSF | Bain Capital Specialty Finance | Financials | 11/15/2018 | 7.5 | $20.25 | $18.00 |

| WEI | Weidai Ltd. | Financials | 11/15/2018 | 4.5 | $10.00 | $10.25 |

| VAPO | Vapotherm | Health Care | 11/14/2018 | 4 | $14.00 | $16.00 |

| ETON | Eton Pharmaceuticals | Health Care | 11/13/2018 | 3.6 | $6.00 | $6.25 |

| CNF | CNFinance Holdings Limited | Financials | 11/7/2018 | 6.5 | $7.50 | $7.60 |

| AXNX | Axonics Modulation Technologies | Health Care | 10/31/2018 | 8 | $15.00 | $14.98 |

| ORTX | Orchard Rx Ltd. | Health Care | 10/31/2018 | 14.3 | $14.00 | $14.00 |

| TWST | Twist Bioscience | Health Care | 10/31/2018 | 5 | $14.00 | $14.00 |

| GMDA | Gamida Cell Ltd. | Health Care | 10/26/2018 | 6.3 | $8.00 | $8.44 |

| PT | Pintec Technology Holdings | Technology | 10/25/2018 | 3.7 | $11.88 | $12.49 |

| YETI | YETI Holdings | Consumer Goods | 10/25/2018 | 16 | $18.00 | $17.00 |

| LOGC | LogicBio Therapeutics | Health Care | 10/19/2018 | 7 | $10.00 | $11.50 |

| NIU | Niu Technologies | Consumer Goods | 10/19/2018 | 7 | $9.00 | $8.65 |

| SWI | SolarWinds | Technology | 10/19/2018 | 25 | $15.00 | $15.03 |

| OSMT | Osmotica Pharmaceuticals plc | Health Care | 10/18/2018 | 6.7 | $7.00 | $8.15 |

| PHAS | PhaseBio Pharmaceuticals | Health Care | 10/18/2018 | 9.2 | $5.00 | $5.00 |

| MSC | Studio City International Holdings | Consumer Services | 10/18/2018 | 28.8 | $12.50 | $15.50 |

| SIBN | SI-BONE | Health Care | 10/17/2018 | 7.2 | $15.00 | $20.06 |

| PLAN | Anaplan | Technology | 10/12/2018 | 15.5 | $17.00 | $24.30 |

| EQ | Equillium | Health Care | 10/12/2018 | 4.7 | $14.00 | $14.00 |

| ALLO | Allogene Therapeutics | Health Care | 10/11/2018 | 18 | $18.00 | $25.00 |

| LTHM | Livent | Basic Materials | 10/11/2018 | 20 | $17.00 | $16.97 |

| ESTC | Elastic N.V. | Technology | 10/5/2018 | 7 | $36.00 | $70.00 |

| GH | Guardant Health | Health Care | 10/4/2018 | 12.5 | $19.00 | $32.20 |

| KOD | Kodiak Sciences Inc. | Health Care | 10/4/2018 | 9 | $10.00 | $10.16 |

| UPWK | Upwork | Technology | 10/3/2018 | 12.5 | $15.00 | $21.18 |

| CTK | CooTek (Cayman) Inc. | Technology | 9/28/2018 | 4.4 | $12.00 | $9.44 |

| ARVN | Arvinas | Health Care | 9/27/2018 | 7.5 | $16.00 | $16.05 |

| LAIX | LAIX Inc. | Consumer Services | 9/27/2018 | 5.8 | $12.50 | $12.65 |

| RMED | Ra Medical Systems | Health Care | 9/27/2018 | 3.9 | $17.00 | $20.00 |

| UROV | Urovant Sciences | Health Care | 9/27/2018 | 10 | $14.00 | $11.65 |

| ARCE | Arco Platform Ltd. | Consumer Services | 9/26/2018 | 11.1 | $17.50 | $23.50 |

| CBNK | Capital Bancorp | Financials | 9/26/2018 | 2.2 | $12.50 | $12.80 |

| ETTX | Entasis Therapeutics Holdings | Health Care | 9/26/2018 | 5 | $15.00 | $10.66 |

| SVMK | SVMK (SurveyMonkey) | Technology | 9/26/2018 | 12 | $12.00 | $17.24 |

| VIOT | Viomi Technology Co., Ltd. | Consumer Goods | 9/25/2018 | 11.4 | $9.00 | $9.08 |

| FTCH | Farfetch Ltd. | Consumer Goods | 9/21/2018 | 44.2 | $20.00 | $28.45 |

| STRO | Sutro Biopharma | Health Care | 9/21/2018 | 5.7 | $15.00 | $15.20 |

| YMAB | Y-mAbs Therapeutics | Health Care | 9/21/2018 | 6 | $16.00 | $24.00 |

| BSVN | Bank7 | Financials | 9/20/2018 | 3.4 | $19.00 | $19.09 |

| ELAN | Elanco Animal Health | Health Care | 9/20/2018 | 62.9 | $24.00 | $36.00 |

| EB | Eventbrite | Technology | 9/20/2018 | 10 | $23.00 | $36.50 |

| XYF | X Financial | Financials | 9/19/2018 | 11 | $9.50 | $11.91 |

| FVCB | FVCBankcorp | Financials | 9/14/2018 | 1.8 | $20.00 | $20.00 |

| PRNB | Principia Biopharma | Health Care | 9/14/2018 | 6.3 | $17.00 | $32.65 |

| QTT | Qutoutiao | Technology | 9/14/2018 | 12 | $7.00 | $15.97 |

| YI | 111 | Consumer Goods | 9/12/2018 | 7.2 | $14.00 | $13.80 |

| NIO | NIO Inc. | Consumer Goods | 9/12/2018 | 160 | $6.26 | $6.60 |

| ARDS | Aridis Pharmaceuticals | Health Care | 8/14/2018 | 2 | $13.00 | $13.00 |

| MESA | Mesa Air Group | Industrials | 8/10/2018 | 9.6 | $12.00 | $11.75 |

| VCNX | Vaccinex | Health Care | 8/9/2018 | 3.3 | $12.00 | $11.38 |

| ARLO | Arlo Technologies | Technology | 8/3/2018 | 10.2 | $16.00 | $22.10 |

| CWK | Cushman & Wakefield plc | Financials | 8/2/2018 | 45 | $17.00 | $17.81 |

| SONO | Sonos | Technology | 8/2/2018 | 13.9 | $15.00 | $19.91 |

| BRY | Berry Petroleum | Health Care | 7/27/2018 | 13 | $14.00 | $13.25 |

| DAVA | Endava Ltd. | Technology | 7/27/2018 | 6.3 | $20.00 | $25.20 |

| OPRA | Opera Ltd. | Technology | 7/27/2018 | 9.6 | $12.00 | $13.11 |

| JG | Aurora Mobile Limited | Technology | 7/26/2018 | 9.1 | $8.50 | $8.80 |

| CANG | Cango | Technology | 7/26/2018 | 4 | $11.00 | $12.52 |

| FOCS | Focus Financial Partners | Financials | 7/26/2018 | 16.2 | $33.00 | $37.55 |

| LQDA | Liquidia Technologies | Health Care | 7/26/2018 | 4.5 | $11.00 | $11.10 |

| PDD | Pinduoduo | Technology | 7/26/2018 | 85.6 | $19.00 | $26.70 |

| TENB | Tenable Holdings | Technology | 7/26/2018 | 10.9 | $23.00 | $30.25 |

| AQST | Aquestive Therapeutics | Health Care | 7/25/2018 | 4 | $15.00 | $16.05 |

| BE | Bloom Energy | Utilities | 7/25/2018 | 18 | $15.00 | $25.00 |

| REPL | Replimune Group | Health Care | 7/20/2018 | 6.7 | $15.00 | $15.16 |

| ALLK | Allakos | Health Care | 7/19/2018 | 7.1 | $18.00 | $31.25 |

| CNST | Constellation Pharmaceuticals | Health Care | 7/19/2018 | 4 | $15.00 | $11.50 |

| ESTA | Establishment Labs Holdings | Health Care | 7/19/2018 | 3.7 | $18.00 | $24.75 |

| MYFW | First Western Financial | Financials | 7/19/2018 | 2 | $19.00 | $19.00 |

| TLRY | Tilray | Health Care | 7/19/2018 | 9 | $17.00 | $22.39 |

| CCB | Coastal Financial | Financials | 7/18/2018 | 2.9 | $14.50 | $16.40 |

| CRNX | Crinetics Pharmaceuticals | Health Care | 7/18/2018 | 6 | $17.00 | $24.51 |

| RUBY | Rubius Therapeutics | Health Care | 7/18/2018 | 10.5 | $23.00 | $24.25 |

| DOMO | Domo | Technology | 6/29/2018 | 9.2 | $21.00 | $27.30 |

| BJ | BJ’s Wholesale Club Holdings | Consumer Goods | 6/28/2018 | 37.5 | $17.00 | $22.00 |

| BV | BrightView Holdings | Consumer Services | 6/28/2018 | 21.3 | $22.00 | $21.40 |

| EVER | EverQuote | Technology | 6/28/2018 | 4.7 | $18.00 | $18.02 |

| FTSV | Forty Seven | Health Care | 6/28/2018 | 7 | $16.00 | $15.05 |

| TBIO | Translate Bio | Health Care | 6/28/2018 | 9.4 | $13.00 | $0.00 |

Subscribe to:

Posts (Atom)